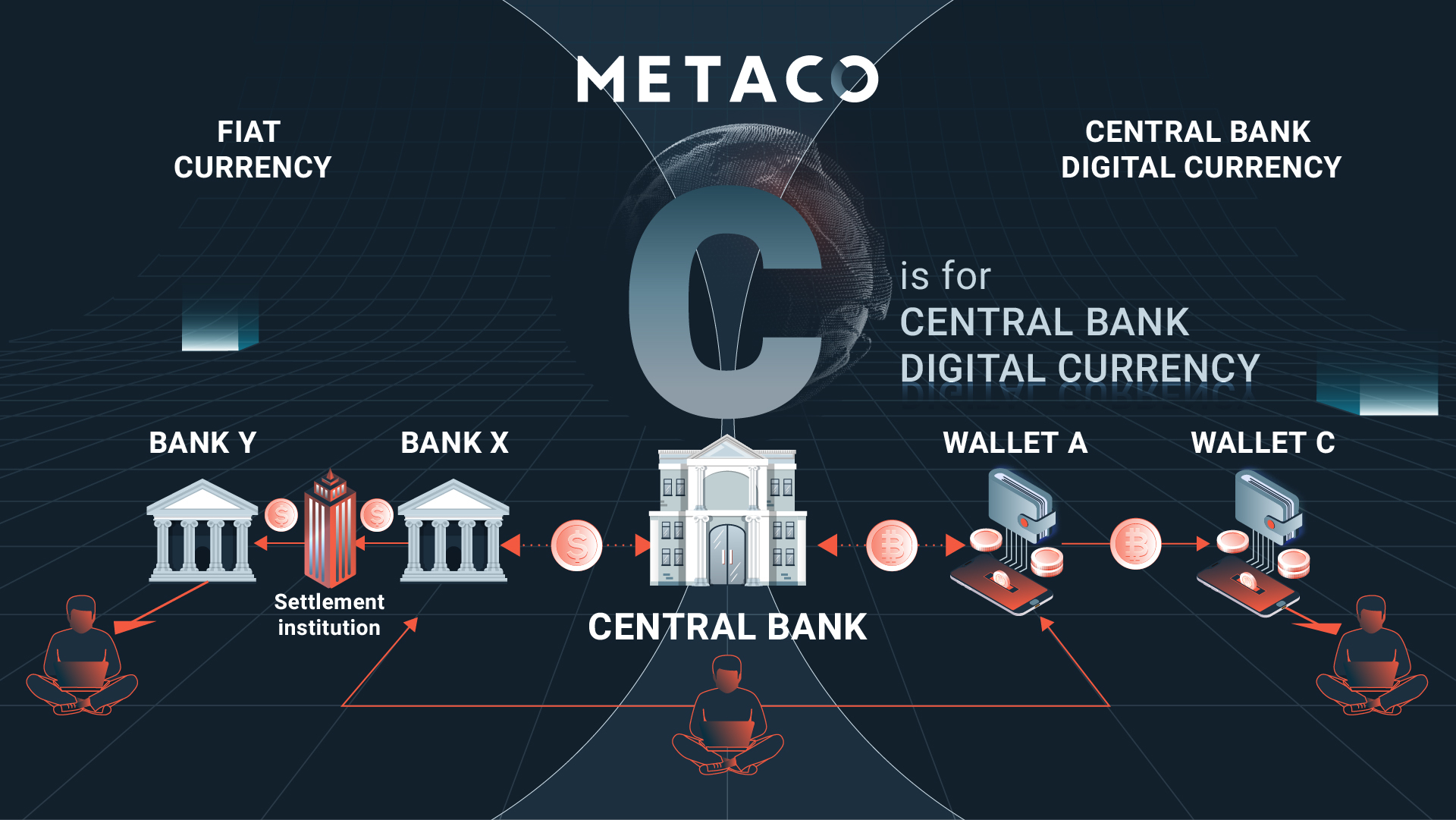

By ALEXANDER MAUNE* Tomorrow belongs to those who can hear it coming. A profound change is taking place before our eyes, a global monetary re-set. This monetary re-set has far-reaching implications - for monetary policy, fiscal policy, and investment decisions. Three key aspects to this change are budgetary nonchalance, the merging of monetary and fiscal policy, and the creation of new tasks for monetary policy. What is meant by monetary climate change/re-set? Ronald-Peter Stoeferle and Mark J. Valek (2021) in their annual report, “In Gold we trust,” refer to it as a multilayered paradigm shift, the breakthrough to which was triggered by the Covid-19 pandemic and the political reactions to it as well as the Ukrainian war. The Covid-19 crisis and the Ukrainian war have the potential to shake up the unbacked monetary system (fiat currency system) and could ultimately shorten its remaining life expectancy significantly. Russia`s response to the economic sanctions imposed by the USA and the EU has shaken the global monetary system and has exposed its weaknesses. To say the least, the sanctions failed to destroy the Russian economy and its currency instead the sanctions strengthened the Russian economy and its currency. Though money has been in existence since time immemorial, very few people seem to appreciate the subject. Money has become controversial the world over. At issue is what constitutes money and its role in economic stability and growth. Disagreements from different schools of thought have ensued regarding the control, supply, and the role of government in money. What is money? James Rickards in his book entitled, “The New Case for Gold,” argues that a classic definition of money has three parts: medium of exchange, store of value, and unit of account. If all three of those criteria are met, you have money of a sort. Rickards states that gold is money, and money has no yield because it has no risk. He further argues that a bank deposit is not money; it is a bank’s unsecured liability. Money should be nothing more than it was at its origin: a market-created good that emerged out of a trade. The most valuable commodity in society, the one good that could be traded for all other goods and thereby help facilitate complex exchange, emerges as money. This could be in the form of beads or animal skins or jewels or precious metals. Gold became money because it had all the properties people look for in good money. The government had nothing to do with it. In 2013 in an interview with BBC`s Justin Rowlatt, Andrea Sella, a Professor of Chemistry at University College London provided an interesting and detailed analysis why gold makes a good currency among the 118 elements in the periodic table. He discounted each element one by one until he was left with gold and silver as the only elements that can make a good currency. Although gold has been acknowledged as real asset, that is money, contemporary wisdom seems to see otherwise with the introduction of central bank digital currency. Central bank digital currency Kraken Intelligence argues that, while the concept of central bank digital currencies (CBDCs) was inspired by cryptocurrencies like bitcoin, the ethos of CBDCs show a stark contrast from the ethos of cryptocurrencies in that they are issued by the state as a centralized form of digital money. Stoeferle and Valek (2021) argue that in the reshaping of the global monetary order, China continues to work on all fronts to undermine the hegemony of the US dollar. In this struggle, China has opened another front, the digital front. While the digital Yuan is already making its first real-world test runs, the Eurozone is only in the early planning stages. According to Bloomberg, among those CBs that have some form of CBDC on their radar, there are currently three zones, apart from the Bahamas, that have already introduced a CBDC in 2020, the ‘Sand Dollar.’ In Asia and South Africa, plans are already fixed and tests with CBDCs are underway. In Europe and Russia, plans are being prepared and CBs have made it clear that they see CBDCs as the future. In the US, the UK, Australia, and Japan – the core countries of the US dollar bloc – CBs are merely experimenting and see no reason to hurry. To Stoeferle and Valek (2021), one aspiration of many CBs is to hastily introduce a CBDC. The CBDCs are a wolf in sheep’s clothing. The Kraken Intelligence (April 2021) publication refers to CBDCs as “digitized fiat currency”. But how possible is a monetary world backed by gold? Russia has proven that it is possible to back a currency by a commodity in this case gold with positive results. A monetary world backed by gold A new monetary world order must be anchored to something tangible. That tangible asset is likely to be gold as in the case of the Russian Ruble. However, it is less likely to be a replica of the old system, but rather gold-backed digital currency centralized by one or several central banks. The Chinese central bank, the People's Bank of China (PBoC) has already launched their CBDC with aspirations to soon be used in international trade settlements and eventually even used as legal tender in jurisdictions outside China and between third-party countries. China may even retain control over their capital and financial accounts whilst internationalizing its digital renminbi. But for it to be trusted in a world with runaway inflation, it is paramount that it is anchored to gold. Why gold? The answer is “True gold fears no fire”. China has long been one of the most important players in the gold market. In 1983, China allowed private gold ownership, but trade was reserved for the PBoC until 2001. Today China is the world's largest gold-producing country, the largest gold consumer, and the largest gold importer. It is argued that not a single gram of gold extracted from the earth in China, or imported by China, leaves the country. Gold is a physical manifestation of money and has emerged throughout human history as the most trustworthy one. Although gold is not currently defined as legal tender, its reputation and trustworthiness as the money remain unblemished. Hence, it should not surprise that the world’s central banks collectively hold 33.919 tonnes or about 17.2% of the world’s gold reserves in their vaults as reserve assets. No fiat currency has survived the test of time. They have all failed to be a reliable store of wealth. French philosopher Voltaire (1729) states that "All paper money eventually returns to its intrinsic value: Zero." To Allan Greenspan, “…Gold is a currency. It is still, by all evidence, a premier currency. No fiat currency, including the dollar, can match it.” Why Gold? Why Now? Stores of wealth sit. Money moves. It travels from one pocket to another. A store of wealth is mass; money is a measurement of wealth. Gold's durability, density, and glow made it a natural choice as a store of wealth long before people thought about using it as money. But why are several African countries with vast gold deposits and other mineral commodities poor and sinking in debt from multilateral institutions like the IMF and the World Bank? In the 16th century the Spanish Parliament or the Cortes gave the answer when it declared, "The more of [gold] that comes in, the less the Kingdom has. ... Though our kingdoms should be the richest in the world ... they are the poorest, for they are only a bridge for [the gold and silver] to go to the Kingdoms of our enemies." In 1608 Pedro de Valencia, wrote "So much silver and money ... always has been fatal poison to republics and cities. They believe money will keep them and it is not true: ploughed fields, pastures, and fisheries are what give sustenance." Instead of transforming the gold and silver into new productive wealth, Africa pays the precious metals out to other countries and spent so much that debts to foreigners soared. We see this happening Africa before our eyes. The Indians seem to be different. As noted by Earl Hamilton an economic historian who stated that India is the largest buyer of gold in the world. India is where gold continues to be the most popular form of portable wealth. Hamilton argues that the Indians spend more on gold than on cars, two-wheeled transport, refrigerators, and colour televisions combined. The Indians are like the Japanese. The Japanese prefer to save their money and accumulate treasure instead of going out and spending it on imports from abroad. One thing is certain: Asians derive much pleasure from their ownership of gold. Gold's natural attributes of malleability, indestructibility, and dazzling beauty appeal to people in any part of the world. Asians are different from Africans. Africans can risk everything to smuggle the precious mineral out of their countries in exchange for paper money. The OR Tambo arrest is one such case. It is so sad that we cannot differentiate real assets from fake assets. But what is an asset? The IASB defines an asset as a resource controlled by the entity [individual] as a result of past events and from which future economic benefits are expected to flow to the entity [individual]. What we fail to understand is that gold remains a definitive mark of opulence. Thus, the mystique of gold as a store of wealth, which is critically dependent on its scarcity, has added lustre to gold as a symbol of power. There was never a time when gold was not in constant demand either for ostentation or for hoarding. Hoarding is similar to buying an insurance policy. Like an insurance policy, hoarding gold has a cost, for the idle metal earns nothing. However, we sleep better knowing that we hold some kind of a hedge against the chance that the catastrophes we fear may occur. This motive is as powerful among poor peasants and labourers as among kings and princes. For 5,000 years, gold has served as humanity’s most effective uncertainty insurance. To Simon Mikhailovich, gold is behaving exactly like insurance should behave – rising and falling with confidence and catastrophic risk perceptions. Dylan Grice argues that confidence in central bankers’ ability to learn from past inflation is as likely to be misplaced …. Gold remains the cleanest insurance against such overconfidence. Metallic money, or paper money convertible into metal, is usually considered to have more value than a system that uses paper only. As Ma Twan-lin reminded us, "Paper should never be money [but] only employed as a representative sign of value existing in metals or produce." The role of gold as the best wealth insurance can never be overemphasized. Recently, the vice-chairman of the Swiss National Bank asserted that "We are convinced that gold will continue to play a role as a currency reserve, especially in times of crisis." In April 1998, the annual report of the Bank of France of 1997 sounded like old times: "Gold remains an element of long-term confidence in the currency.... Above all, holding gold is, from the political point of view, a sign of monetary sovereignty [and] an insurance policy against a major breakdown in the international monetary system." About the same time, a former managing director of the IMF affirmed that "Gold remains at the heart of a collective belief in the credibility of an international economy ... a sort of `war chest,' indispensable for a tomorrow whose needs we can only guess." Why gold? Every piece of gold reflects the same qualities. All the gold in the world is all made of the same stuff. Gold`s chemical symbol AU derives from Aurora, which means "shining dawn," but despite the glamorous suggestion of AU, gold is chemically inert. That explains why its radiance is forever. In Cairo, we will find a tooth bridge made of gold for an Egyptian 4500 years ago, its condition good enough to go into our mouth today. Gold is almost as soft as putty. The gold on Venetian glasses was hammered down to as little as five millionths of an inch-a process known as gilding. We could draw an ounce of gold into a wire fifty miles in length, or, if we prefer, we could beat that ounce into a sheet that would cover one hundred square feet. Unlike any other element on earth, almost all the gold ever mined is still around. But in comparison with steel, gold seems to play an insignificant role, especially in industry. We can further argue that out of steel, we build office towers, ships, automobiles, containers, and machinery of all types; out of gold, we build nothing. And yet it is gold that we call the precious metal. We yearn for gold and yawn at steel. Why then Gold? When all the steel has rusted and rotted, and forever after that, gold will still look like new. That is the kind of longevity we all dream of. Gold may be volatile when measured in nominal dollars. Still, the volatility has more to do with the value of the dollar than with the value of gold. Historically, gold has done well in inflation and deflation because it represents a real store of value. Savers of paper money are the biggest losers given the prevailing financial environment. It's high time we change our mindsets and wake up to the realities of life and start investing in real assets. Gold is one of those real assets that has been tried and tested as the best wealth insurance. *Alexander Maune is a lecturer, Talmudic scholar, researcher, and consultant as well as a member of IoDZ. Mailto: alexandermaune6@gmail.com.

Tomorrow belongs to those who can hear it coming. A profound change is taking place before our eyes, a global monetary re-set. This monetary re-set has far-reaching implications - for monetary policy, fiscal policy, and investment decisions. Three key aspects to this change are budgetary nonchalance, the merging of monetary and fiscal policy, and the creation of new tasks for monetary policy. What is meant by monetary climate change/re-set? Ronald-Peter Stoeferle and Mark J. Valek (2021) in their annual report, “In Gold we trust,” refer to it as a multilayered paradigm shift, the breakthrough to which was triggered by the Covid-19 pandemic and the political reactions to it as well as the Ukrainian war. The Covid-19 crisis and the Ukrainian war have the potential to shake up the unbacked monetary system (fiat currency system) and could ultimately shorten its remaining life expectancy significantly. Russia`s response to the economic sanctions imposed by the USA and the EU has shaken the global monetary system and has exposed its weaknesses. To say the least, the sanctions failed to destroy the Russian economy and its currency instead the sanctions strengthened the Russian economy and its currency. Though money has been in existence since time immemorial, very few people seem to appreciate the subject. Money has become controversial the world over. At issue is what constitutes money and its role in economic stability and growth. Disagreements from different schools of thought have ensued regarding the control, supply, and the role of government in money. What is money? James Rickards in his book entitled, “The New Case for Gold,” argues that a classic definition of money has three parts: medium of exchange, store of value, and unit of account. If all three of those criteria are met, you have money of a sort. Rickards states that gold is money, and money has no yield because it has no risk. He further argues that a bank deposit is not money; it is a bank’s unsecured liability. Money should be nothing more than it was at its origin: a market-created good that emerged out of a trade. The most valuable commodity in society, the one good that could be traded for all other goods and thereby help facilitate complex exchange, emerges as money. This could be in the form of beads or animal skins or jewels or precious metals. Gold became money because it had all the properties people look for in good money. The government had nothing to do with it. In 2013 in an interview with BBC`s Justin Rowlatt, Andrea Sella, a Professor of Chemistry at University College London provided an interesting and detailed analysis why gold makes a good currency among the 118 elements in the periodic table. He discounted each element one by one until he was left with gold and silver as the only elements that can make a good currency. Although gold has been acknowledged as real asset, that is money, contemporary wisdom seems to see otherwise with the introduction of central bank digital currency. Central bank digital currency Kraken Intelligence argues that, while the concept of central bank digital currencies (CBDCs) was inspired by cryptocurrencies like bitcoin, the ethos of CBDCs show a stark contrast from the ethos of cryptocurrencies in that they are issued by the state as a centralized form of digital money. Stoeferle and Valek (2021) argue that in the reshaping of the global monetary order, China continues to work on all fronts to undermine the hegemony of the US dollar. In this struggle, China has opened another front, the digital front. While the digital Yuan is already making its first real-world test runs, the Eurozone is only in the early planning stages. According to Bloomberg, among those CBs that have some form of CBDC on their radar, there are currently three zones, apart from the Bahamas, that have already introduced a CBDC in 2020, the ‘Sand Dollar.’ In Asia and South Africa, plans are already fixed and tests with CBDCs are underway. In Europe and Russia, plans are being prepared and CBs have made it clear that they see CBDCs as the future. In the US, the UK, Australia, and Japan – the core countries of the US dollar bloc – CBs are merely experimenting and see no reason to hurry. To Stoeferle and Valek (2021), one aspiration of many CBs is to hastily introduce a CBDC. The CBDCs are a wolf in sheep’s clothing. The Kraken Intelligence (April 2021) publication refers to CBDCs as “digitized fiat currency”. But how possible is a monetary world backed by gold? Russia has proven that it is possible to back a currency by a commodity in this case gold with positive results. A monetary world backed by gold A new monetary world order must be anchored to something tangible. That tangible asset is likely to be gold as in the case of the Russian Ruble. However, it is less likely to be a replica of the old system, but rather gold-backed digital currency centralized by one or several central banks. The Chinese central bank, the People's Bank of China (PBoC) has already launched their CBDC with aspirations to soon be used in international trade settlements and eventually even used as legal tender in jurisdictions outside China and between third-party countries. China may even retain control over their capital and financial accounts whilst internationalizing its digital renminbi. But for it to be trusted in a world with runaway inflation, it is paramount that it is anchored to gold. Why gold? The answer is “True gold fears no fire”. China has long been one of the most important players in the gold market. In 1983, China allowed private gold ownership, but trade was reserved for the PBoC until 2001. Today China is the world's largest gold-producing country, the largest gold consumer, and the largest gold importer. It is argued that not a single gram of gold extracted from the earth in China, or imported by China, leaves the country. Gold is a physical manifestation of money and has emerged throughout human history as the most trustworthy one. Although gold is not currently defined as legal tender, its reputation and trustworthiness as the money remain unblemished. Hence, it should not surprise that the world’s central banks collectively hold 33.919 tonnes or about 17.2% of the world’s gold reserves in their vaults as reserve assets. No fiat currency has survived the test of time. They have all failed to be a reliable store of wealth. French philosopher Voltaire (1729) states that "All paper money eventually returns to its intrinsic value: Zero." To Allan Greenspan, “…Gold is a currency. It is still, by all evidence, a premier currency. No fiat currency, including the dollar, can match it.” Why Gold? Why Now? Stores of wealth sit. Money moves. It travels from one pocket to another. A store of wealth is mass; money is a measurement of wealth. Gold's durability, density, and glow made it a natural choice as a store of wealth long before people thought about using it as money. But why are several African countries with vast gold deposits and other mineral commodities poor and sinking in debt from multilateral institutions like the IMF and the World Bank? In the 16th century the Spanish Parliament or the Cortes gave the answer when it declared, "The more of [gold] that comes in, the less the Kingdom has. ... Though our kingdoms should be the richest in the world ... they are the poorest, for they are only a bridge for [the gold and silver] to go to the Kingdoms of our enemies." In 1608 Pedro de Valencia, wrote "So much silver and money ... always has been fatal poison to republics and cities. They believe money will keep them and it is not true: ploughed fields, pastures, and fisheries are what give sustenance." Instead of transforming the gold and silver into new productive wealth, Africa pays the precious metals out to other countries and spent so much that debts to foreigners soared. We see this happening Africa before our eyes. The Indians seem to be different. As noted by Earl Hamilton an economic historian who stated that India is the largest buyer of gold in the world. India is where gold continues to be the most popular form of portable wealth. Hamilton argues that the Indians spend more on gold than on cars, two-wheeled transport, refrigerators, and colour televisions combined. The Indians are like the Japanese. The Japanese prefer to save their money and accumulate treasure instead of going out and spending it on imports from abroad. One thing is certain: Asians derive much pleasure from their ownership of gold. Gold's natural attributes of malleability, indestructibility, and dazzling beauty appeal to people in any part of the world. Asians are different from Africans. Africans can risk everything to smuggle the precious mineral out of their countries in exchange for paper money. The OR Tambo arrest is one such case. It is so sad that we cannot differentiate real assets from fake assets. But what is an asset? The IASB defines an asset as a resource controlled by the entity [individual] as a result of past events and from which future economic benefits are expected to flow to the entity [individual]. What we fail to understand is that gold remains a definitive mark of opulence. Thus, the mystique of gold as a store of wealth, which is critically dependent on its scarcity, has added lustre to gold as a symbol of power. There was never a time when gold was not in constant demand either for ostentation or for hoarding. Hoarding is similar to buying an insurance policy. Like an insurance policy, hoarding gold has a cost, for the idle metal earns nothing. However, we sleep better knowing that we hold some kind of a hedge against the chance that the catastrophes we fear may occur. This motive is as powerful among poor peasants and labourers as among kings and princes. For 5,000 years, gold has served as humanity’s most effective uncertainty insurance. To Simon Mikhailovich, gold is behaving exactly like insurance should behave – rising and falling with confidence and catastrophic risk perceptions. Dylan Grice argues that confidence in central bankers’ ability to learn from past inflation is as likely to be misplaced …. Gold remains the cleanest insurance against such overconfidence. Metallic money, or paper money convertible into metal, is usually considered to have more value than a system that uses paper only. As Ma Twan-lin reminded us, "Paper should never be money [but] only employed as a representative sign of value existing in metals or produce." The role of gold as the best wealth insurance can never be overemphasized. Recently, the vice-chairman of the Swiss National Bank asserted that "We are convinced that gold will continue to play a role as a currency reserve, especially in times of crisis." In April 1998, the annual report of the Bank of France of 1997 sounded like old times: "Gold remains an element of long-term confidence in the currency.... Above all, holding gold is, from the political point of view, a sign of monetary sovereignty [and] an insurance policy against a major breakdown in the international monetary system." About the same time, a former managing director of the IMF affirmed that "Gold remains at the heart of a collective belief in the credibility of an international economy ... a sort of `war chest,' indispensable for a tomorrow whose needs we can only guess." Why gold? Every piece of gold reflects the same qualities. All the gold in the world is all made of the same stuff. Gold`s chemical symbol AU derives from Aurora, which means "shining dawn," but despite the glamorous suggestion of AU, gold is chemically inert. That explains why its radiance is forever. In Cairo, we will find a tooth bridge made of gold for an Egyptian 4500 years ago, its condition good enough to go into our mouth today. Gold is almost as soft as putty. The gold on Venetian glasses was hammered down to as little as five millionths of an inch-a process known as gilding. We could draw an ounce of gold into a wire fifty miles in length, or, if we prefer, we could beat that ounce into a sheet that would cover one hundred square feet. Unlike any other element on earth, almost all the gold ever mined is still around. But in comparison with steel, gold seems to play an insignificant role, especially in industry. We can further argue that out of steel, we build office towers, ships, automobiles, containers, and machinery of all types; out of gold, we build nothing. And yet it is gold that we call the precious metal. We yearn for gold and yawn at steel. Why then Gold? When all the steel has rusted and rotted, and forever after that, gold will still look like new. That is the kind of longevity we all dream of. Gold may be volatile when measured in nominal dollars. Still, the volatility has more to do with the value of the dollar than with the value of gold. Historically, gold has done well in inflation and deflation because it represents a real store of value. Savers of paper money are the biggest losers given the prevailing financial environment. It's high time we change our mindsets and wake up to the realities of life and start investing in real assets. Gold is one of those real assets that has been tried and tested as the best wealth insurance. *Alexander Maune is a lecturer, Talmudic scholar, researcher, and consultant as well as a member of IoDZ. Mailto:

Tomorrow belongs to those who can hear it coming. A profound change is taking place before our eyes, a global monetary re-set. This monetary re-set has far-reaching implications - for monetary policy, fiscal policy, and investment decisions. Three key aspects to this change are budgetary nonchalance, the merging of monetary and fiscal policy, and the creation of new tasks for monetary policy. What is meant by monetary climate change/re-set? Ronald-Peter Stoeferle and Mark J. Valek (2021) in their annual report, “In Gold we trust,” refer to it as a multilayered paradigm shift, the breakthrough to which was triggered by the Covid-19 pandemic and the political reactions to it as well as the Ukrainian war. The Covid-19 crisis and the Ukrainian war have the potential to shake up the unbacked monetary system (fiat currency system) and could ultimately shorten its remaining life expectancy significantly. Russia`s response to the economic sanctions imposed by the USA and the EU has shaken the global monetary system and has exposed its weaknesses. To say the least, the sanctions failed to destroy the Russian economy and its currency instead the sanctions strengthened the Russian economy and its currency. Though money has been in existence since time immemorial, very few people seem to appreciate the subject. Money has become controversial the world over. At issue is what constitutes money and its role in economic stability and growth. Disagreements from different schools of thought have ensued regarding the control, supply, and the role of government in money. What is money? James Rickards in his book entitled, “The New Case for Gold,” argues that a classic definition of money has three parts: medium of exchange, store of value, and unit of account. If all three of those criteria are met, you have money of a sort. Rickards states that gold is money, and money has no yield because it has no risk. He further argues that a bank deposit is not money; it is a bank’s unsecured liability. Money should be nothing more than it was at its origin: a market-created good that emerged out of a trade. The most valuable commodity in society, the one good that could be traded for all other goods and thereby help facilitate complex exchange, emerges as money. This could be in the form of beads or animal skins or jewels or precious metals. Gold became money because it had all the properties people look for in good money. The government had nothing to do with it. In 2013 in an interview with BBC`s Justin Rowlatt, Andrea Sella, a Professor of Chemistry at University College London provided an interesting and detailed analysis why gold makes a good currency among the 118 elements in the periodic table. He discounted each element one by one until he was left with gold and silver as the only elements that can make a good currency. Although gold has been acknowledged as real asset, that is money, contemporary wisdom seems to see otherwise with the introduction of central bank digital currency. Central bank digital currency Kraken Intelligence argues that, while the concept of central bank digital currencies (CBDCs) was inspired by cryptocurrencies like bitcoin, the ethos of CBDCs show a stark contrast from the ethos of cryptocurrencies in that they are issued by the state as a centralized form of digital money. Stoeferle and Valek (2021) argue that in the reshaping of the global monetary order, China continues to work on all fronts to undermine the hegemony of the US dollar. In this struggle, China has opened another front, the digital front. While the digital Yuan is already making its first real-world test runs, the Eurozone is only in the early planning stages. According to Bloomberg, among those CBs that have some form of CBDC on their radar, there are currently three zones, apart from the Bahamas, that have already introduced a CBDC in 2020, the ‘Sand Dollar.’ In Asia and South Africa, plans are already fixed and tests with CBDCs are underway. In Europe and Russia, plans are being prepared and CBs have made it clear that they see CBDCs as the future. In the US, the UK, Australia, and Japan – the core countries of the US dollar bloc – CBs are merely experimenting and see no reason to hurry. To Stoeferle and Valek (2021), one aspiration of many CBs is to hastily introduce a CBDC. The CBDCs are a wolf in sheep’s clothing. The Kraken Intelligence (April 2021) publication refers to CBDCs as “digitized fiat currency”. But how possible is a monetary world backed by gold? Russia has proven that it is possible to back a currency by a commodity in this case gold with positive results. A monetary world backed by gold A new monetary world order must be anchored to something tangible. That tangible asset is likely to be gold as in the case of the Russian Ruble. However, it is less likely to be a replica of the old system, but rather gold-backed digital currency centralized by one or several central banks. The Chinese central bank, the People's Bank of China (PBoC) has already launched their CBDC with aspirations to soon be used in international trade settlements and eventually even used as legal tender in jurisdictions outside China and between third-party countries. China may even retain control over their capital and financial accounts whilst internationalizing its digital renminbi. But for it to be trusted in a world with runaway inflation, it is paramount that it is anchored to gold. Why gold? The answer is “True gold fears no fire”. China has long been one of the most important players in the gold market. In 1983, China allowed private gold ownership, but trade was reserved for the PBoC until 2001. Today China is the world's largest gold-producing country, the largest gold consumer, and the largest gold importer. It is argued that not a single gram of gold extracted from the earth in China, or imported by China, leaves the country. Gold is a physical manifestation of money and has emerged throughout human history as the most trustworthy one. Although gold is not currently defined as legal tender, its reputation and trustworthiness as the money remain unblemished. Hence, it should not surprise that the world’s central banks collectively hold 33.919 tonnes or about 17.2% of the world’s gold reserves in their vaults as reserve assets. No fiat currency has survived the test of time. They have all failed to be a reliable store of wealth. French philosopher Voltaire (1729) states that "All paper money eventually returns to its intrinsic value: Zero." To Allan Greenspan, “…Gold is a currency. It is still, by all evidence, a premier currency. No fiat currency, including the dollar, can match it.” Why Gold? Why Now? Stores of wealth sit. Money moves. It travels from one pocket to another. A store of wealth is mass; money is a measurement of wealth. Gold's durability, density, and glow made it a natural choice as a store of wealth long before people thought about using it as money. But why are several African countries with vast gold deposits and other mineral commodities poor and sinking in debt from multilateral institutions like the IMF and the World Bank? In the 16th century the Spanish Parliament or the Cortes gave the answer when it declared, "The more of [gold] that comes in, the less the Kingdom has. ... Though our kingdoms should be the richest in the world ... they are the poorest, for they are only a bridge for [the gold and silver] to go to the Kingdoms of our enemies." In 1608 Pedro de Valencia, wrote "So much silver and money ... always has been fatal poison to republics and cities. They believe money will keep them and it is not true: ploughed fields, pastures, and fisheries are what give sustenance." Instead of transforming the gold and silver into new productive wealth, Africa pays the precious metals out to other countries and spent so much that debts to foreigners soared. We see this happening Africa before our eyes. The Indians seem to be different. As noted by Earl Hamilton an economic historian who stated that India is the largest buyer of gold in the world. India is where gold continues to be the most popular form of portable wealth. Hamilton argues that the Indians spend more on gold than on cars, two-wheeled transport, refrigerators, and colour televisions combined. The Indians are like the Japanese. The Japanese prefer to save their money and accumulate treasure instead of going out and spending it on imports from abroad. One thing is certain: Asians derive much pleasure from their ownership of gold. Gold's natural attributes of malleability, indestructibility, and dazzling beauty appeal to people in any part of the world. Asians are different from Africans. Africans can risk everything to smuggle the precious mineral out of their countries in exchange for paper money. The OR Tambo arrest is one such case. It is so sad that we cannot differentiate real assets from fake assets. But what is an asset? The IASB defines an asset as a resource controlled by the entity [individual] as a result of past events and from which future economic benefits are expected to flow to the entity [individual]. What we fail to understand is that gold remains a definitive mark of opulence. Thus, the mystique of gold as a store of wealth, which is critically dependent on its scarcity, has added lustre to gold as a symbol of power. There was never a time when gold was not in constant demand either for ostentation or for hoarding. Hoarding is similar to buying an insurance policy. Like an insurance policy, hoarding gold has a cost, for the idle metal earns nothing. However, we sleep better knowing that we hold some kind of a hedge against the chance that the catastrophes we fear may occur. This motive is as powerful among poor peasants and labourers as among kings and princes. For 5,000 years, gold has served as humanity’s most effective uncertainty insurance. To Simon Mikhailovich, gold is behaving exactly like insurance should behave – rising and falling with confidence and catastrophic risk perceptions. Dylan Grice argues that confidence in central bankers’ ability to learn from past inflation is as likely to be misplaced …. Gold remains the cleanest insurance against such overconfidence. Metallic money, or paper money convertible into metal, is usually considered to have more value than a system that uses paper only. As Ma Twan-lin reminded us, "Paper should never be money [but] only employed as a representative sign of value existing in metals or produce." The role of gold as the best wealth insurance can never be overemphasized. Recently, the vice-chairman of the Swiss National Bank asserted that "We are convinced that gold will continue to play a role as a currency reserve, especially in times of crisis." In April 1998, the annual report of the Bank of France of 1997 sounded like old times: "Gold remains an element of long-term confidence in the currency.... Above all, holding gold is, from the political point of view, a sign of monetary sovereignty [and] an insurance policy against a major breakdown in the international monetary system." About the same time, a former managing director of the IMF affirmed that "Gold remains at the heart of a collective belief in the credibility of an international economy ... a sort of `war chest,' indispensable for a tomorrow whose needs we can only guess." Why gold? Every piece of gold reflects the same qualities. All the gold in the world is all made of the same stuff. Gold`s chemical symbol AU derives from Aurora, which means "shining dawn," but despite the glamorous suggestion of AU, gold is chemically inert. That explains why its radiance is forever. In Cairo, we will find a tooth bridge made of gold for an Egyptian 4500 years ago, its condition good enough to go into our mouth today. Gold is almost as soft as putty. The gold on Venetian glasses was hammered down to as little as five millionths of an inch-a process known as gilding. We could draw an ounce of gold into a wire fifty miles in length, or, if we prefer, we could beat that ounce into a sheet that would cover one hundred square feet. Unlike any other element on earth, almost all the gold ever mined is still around. But in comparison with steel, gold seems to play an insignificant role, especially in industry. We can further argue that out of steel, we build office towers, ships, automobiles, containers, and machinery of all types; out of gold, we build nothing. And yet it is gold that we call the precious metal. We yearn for gold and yawn at steel. Why then Gold? When all the steel has rusted and rotted, and forever after that, gold will still look like new. That is the kind of longevity we all dream of. Gold may be volatile when measured in nominal dollars. Still, the volatility has more to do with the value of the dollar than with the value of gold. Historically, gold has done well in inflation and deflation because it represents a real store of value. Savers of paper money are the biggest losers given the prevailing financial environment. It's high time we change our mindsets and wake up to the realities of life and start investing in real assets. Gold is one of those real assets that has been tried and tested as the best wealth insurance. *Alexander Maune is a lecturer, Talmudic scholar, researcher, and consultant as well as a member of IoDZ. Mailto: